Want to know what your property is worth?

Want to know what your property is worth?

If you have ever considered building a property portfolio as a landlord, now could be a great time to start your journey.

Information from a market-leading property portal indicates rents have risen at the fastest rate on record, and tenant demand has almost doubled. At a time when interest rates on traditional savings accounts are low, many believe it is a good time to invest in the property market. *

Lenders are evidently committed to supporting prospective landlords. A recent report from a popular money comparison site revealed there are currently 2,235 mortgage products on offer to first-time landlords, an increase of more than 70% than the same time last year.

A huge 64% of available buy-to-let mortgage products are catering to first-time investors and rates are attractive, allowing landlords to protect themselves against future rate rises by locking into a good deal with a fixed-rate mortgage. The average two-year fixed rate mortgage for a first-time landlord is currently 3.19%, rising to 3.47% for a five-year fixed product.

If you would like to explore buy-to-let properties and mortgage products which could lay the foundations for your property portfolio, call us today and talk to one of our team members.

Last year, Rightmove saw a 26% increase in web traffic, with over four million of us visiting their website on Boxing Day.

Your property could be marketed to a HUGE online audience over the festive period and the New Year.

Listing is a sure-fire way of capturing attention from serious buyers and tenants.

Did you know...

Online property searches double over the Christmas and New Year period.

On average, there's a 20% increase in people searching online for their next home.

9 pm was the citied as last year's prime property-surfing time.

Over 2.3 million people visit Rightmove on the 29th December.

Over 3.3. million people visit Rightmove on the first day of the New Year.

Taking a step on the ladder is really exciting!

So, you shouldn’t be daunted by mortgages. We can help you find your perfect property and offer you expert mortgage advice.

What is a fixed-rate mortgage?

With a fixed-rate mortgage, the interest rate that you pay remains the same throughout the period of the contract – typically one to five years. Choosing a fixed-rate mortgage means that you will know exactly how much your mortgages will cost for a set period of time, and your repayments will remain the same, even if interest rates change.

What is a tracker mortgage?

The interest rate on a tracker mortgage is linked to the Bank of England base rate. This means that if the base rate changes, so will your mortgage rate. You can get lifetime or term trackers that are often very flexible and can be great if you don’t want to be tied into a mortgage.

What is a guarantor mortgage?

With a guarantor mortgage, your friends or family members can opt to be your mortgage guarantor. With this type of mortgage, if you miss any repayments, your guarantor could risk losing their savings or their home.

This article was extracted from Rightmove for informational purposes

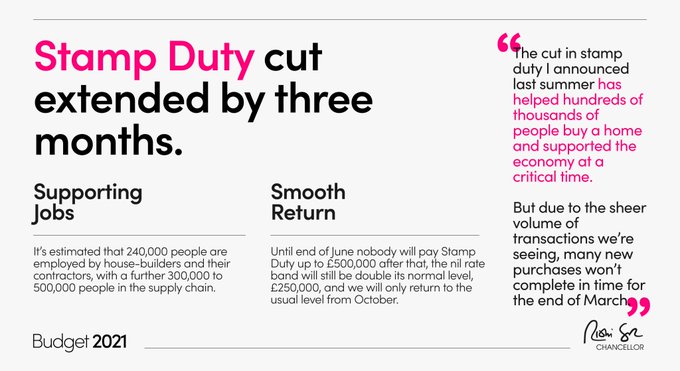

The government has announced that the temporary stamp duty holiday in England and Northern Ireland has been extended until the end of June.

The news will hopefully come as a relief to those buyers and sellers who have been desperately trying to get their sale completed in time to meet the previous deadline of 31st March.

What is the temporary stamp duty holiday?

The temporary stamp duty holiday, first announced by the government on 8th July last year, means that if you are buying a home up to the value of £500,000 you will not pay any stamp duty.

The extension means you now have until 30th June to complete on the purchase to make the stamp duty saving.

Then, to smooth the transition back to normal, the nil rate band will be £250,000, double its standard level, until the end of September.

It will return to the usual threshold of £125,000 on 1st October.

There hasn’t been any further update from Scotland on any extension to the Land & Buildings Transaction Tax (LBTT) holiday, which is currently due to end on 31st March 2021.

In Wales, temporary Land Transaction Tax reductions are also set to end on 31st March, but we’ll let you know if this changes.

Are there delays in the home-moving process right now?

When the announcement was first made in July we recorded our busiest ever day on Rightmove, as people rushed to see if they could move home and make use of the savings, leading to a huge increase in the usual number of sales that would be going through the legal process.

We estimate that there are currently 628,000 sales going through, and this massive number, coupled with the challenges of conveyancers, solicitors and councils working from home, has led to delays in the home-buying process.

Our latest data shows that it is taking an average of 65 days from the time a seller has a property listed by an agent on Rightmove until they get an offer accepted, and a further 126 days to get through to legal completion, which is almost seven months.

But remember these are averages, and other factors such as if you are a cash buyer or if council searches in your area take longer will affected how long it takes.

What do the experts say?

Our resident property data expert Tim Bannister explained that the stamp duty holiday extension should give tens of thousands of home-movers the chance to complete before the new deadline.

He said: “This three-month extension will come as a huge relief for those people who have been going through the sales process since last year and were always expecting to make use of the stamp duty savings.

“Our recent data shows one in five sales that were agreed in the same month the stamp duty holiday was first announced in July last year still haven’t completed, so this additional time will make a big difference to help those stuck in the logjam complete their purchase in time before the new end of June deadline.

“Buyers who have recently agreed a sale now have a race on their hands to see if they can also make use of the stamp duty savings, but many with purchases over £250,000 will find that time is too tight to complete before the end of June and so shouldn’t be factoring this into their purchase.

“It’s worth remembering that the average savings vary massively around England, and first-time buyers will still be exempt if they’re buying for £300,000 or less. There are also many other reasons people are choosing to move, evidenced by the strong buyer demand Rightmove has already seen in the first two months of the year.”

The following information is extracted from Rightmove

A mortgage guarantee scheme aimed at helping first-time buyers and existing homeowners is set to be unveiled by the government in this week’s Spring Budget announcement.

Chancellor Rishi Sunak is expected to reveal the specifics of the scheme on Wednesday (3rd March). In the meantime, we can share what we know so far.

What do we know about the mortgage guarantee scheme?

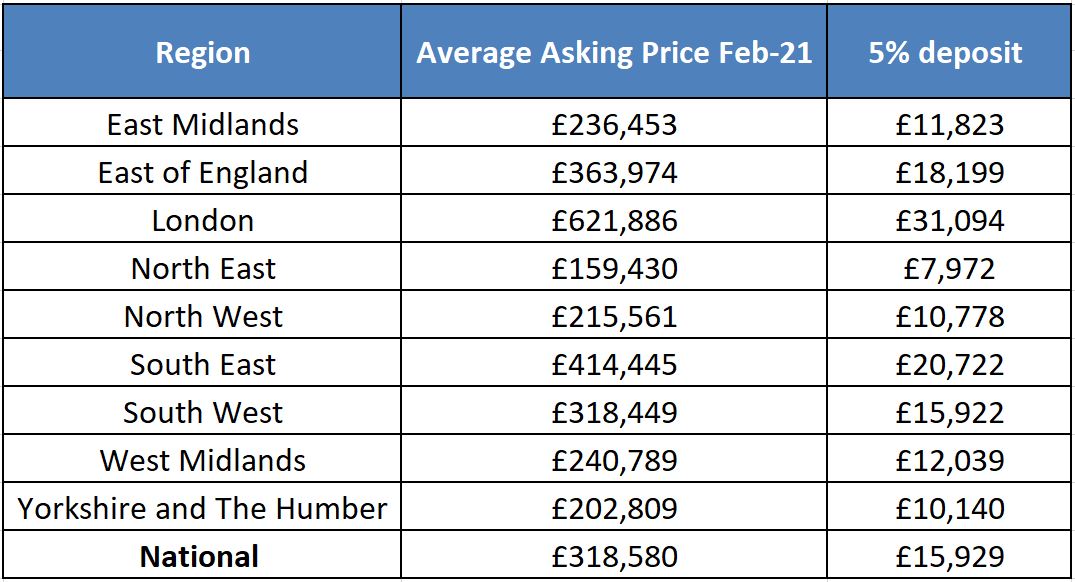

Under the new scheme, which is expected to launch in April, we anticipate that buyers will be able to purchase homes worth up to £600,000 with a deposit of just 5%.

And this means that the majority of buyers should be eligible for the scheme, as our data analysts have found that 86% of properties currently listed for sale on our site have an asking price of £600,000 or less.

However, please note that with an average asking price of £621,886, many properties across Greater London will be priced above the scheme’s proposed threshold of £600,000 (see below).

What impact could the mortgage guarantee scheme have regionally?

What are some of the key statistics?

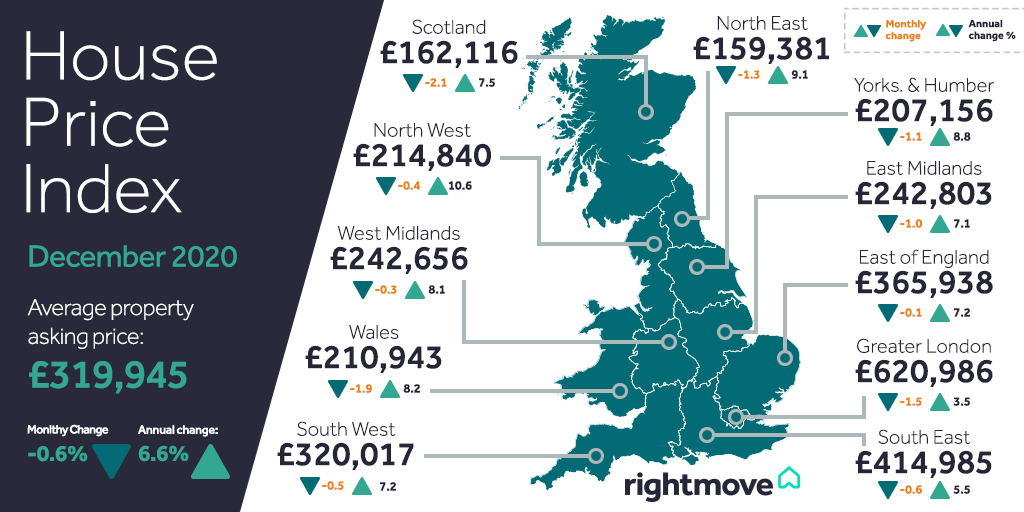

- The national average asking price for all properties is currently £318,580, which is 3.0% higher than February 2020

- The national average asking price of a first-time buyer property is £200,692, which is 3.6% higher than February 2020

- Since the 2013 Help to Buy mortgage guarantee scheme was first launched, national asking prices have increased by 29% from £246,748 in October 2013 to £318,580 in February 2021

- Since the 2013 Help to Buy mortgage guarantee scheme was first launched, national asking prices for first-time buyer properties have increased by 36% from £147,464 in October 2013 to £200,692 in February 2021

The rent or buy debate is a pretty controversial topic with no simple answer, but we want to put paid to the ever-present myth that buying is always better than renting.

But renting doesn’t mean you are throwing away money in the same way that buying a home isn’t always the right decision at certain times in your life. So we’ve come up with a list of 12 reasons why renting might just be the better option for you.

1.No maintenance costs or repair bills

When renting a property, your landlord is usually responsible for all maintenance and repair costs, ensuring you don’t have the financial responsibility to get these things fixed.

2. No large down-payment

Renters have the better financial deal upon signing as a house with a mortgage requires a sizable down payment compared to the usual deposit for renting a property.

3. There’s a fixed rent amount

Rent amounts are certain for the span of the lease agreement – so long as it’s a fixed-term contract – making it easier to budget your money so you know exactly how much you’re required to pay.

4. You can keep things flexible!

When you buy a house you are tied down to living in that location for at least a few years usually, whereas if you’re renting a property you have the flexibility to move around if something changes in your life or outlook.

5. You have the options for housemates

Housemates are many things – from being someone to split the bills with to potentially becoming some of the best friendships you may ever have.

6. Invest money on your own terms

Choosing not to buy a home – at least for the moment – opens up other possibilities for saving and investing so you can choose exactly where your hard-earned money is going.

7. Generally lower utility costs

Rental properties typically have a more compact floor plan, therefore renters can often expect to face lower utility costs – another money saver.

8. Enjoy being mortgage-free

By renting you can put away as much (or more) savings as a homeowner, but without the debt that comes along with owning a property.

9. Urban living at a cheaper price

Depending on where you want to live, trendy areas, such as major cities, and beach communities, are typically more renter friendly.

10. Decreasing property value

Property values go up and down over the years depending on the area you live, and, while this may affect homeowners in a big way, it affects renters substantially less so, if at all.

11. Excuse yourself from costly updates

As a renter, there is freedom in knowing you couldn’t remodel your home even if you wanted to, so this a way of saving money.

12. Insurance is cheaper

Renter’s insurance is significantly cheaper than the insurance home owners have to pay.

So there you have it. It’s likely you already have your own opinion about whether renting or buying is right for you now – or in the future – but hopefully this article has given you a few reasons to show that renting can be seriously advantageous for many of us.

If you are considering selling or letting your property in Ashtead, Leatherhead, Fetcham, Epsom, Bookham or the surrounding areas, call V&H Homes on 01372 221 678

The following information has been extracted from Rightmove

Choose the right estate agent

If you haven’t had your property valued yet, get that booked in as soon as possible. We recommend you get at least two agents around to value your home, and choosing the right for you is super important.

Here’s a list to help you know what to look for:

- How experienced are they in your area?

- Have they successfully sold properties similar to yours recently? Find out how long it took them, what prices were achieved, and what the difference between their initial asking price and the sold price was, if any.

- Don’t become overly fixated with the fee the agent charges. Usually the most important things to keep in mind are:

- The amount of money the house sells for: the sold price minus the agent’s fee.

- How quickly the sale will happen.

Working with an agent who provides a great service, is responsive, proactive, and an expert in your local area, will make a huge difference to the whole experience, and is most likely to get your house on the market quicker.

Get the price right

Don’t automatically be swayed by the agent promising the highest price for your home. It’s tempting, but if you end up over-pricing the property it will only prolong the process, and you’ll have to reduce the price further down the line anyway. A recent study we carried out found that you were twice as likely to sell your home if it sold based on the first listed asking price.

Instead, ask the agent to provide evidence to support why they recommend that asking price. And again, look at their recent history in the area.

The first two weeks your house appears on Rightmove is usually when it gets the most attention from home-hunters – especially during this busy period. So if it’s priced correctly, with the level of exposure it could be getting, you may even end up with an offer in the first couple of weeks.

Have all documents ready

Your estate agent and solicitor will ask for various bits of paperwork throughout the selling process, so if you can gather together all the relevant documents ahead of time, you should avoid delays further down the line.

Some of the paperwork to consider rounding up include:

- HM Land Registry title documents

- gas checks completed by a Gas Safe registered engineer (or Corgi-registered engineer prior to 2009)

- electrical checks – an Electrical Installation Condition Report (EICR) or a NAPIT or NICEIC certificate/report from a registered electrical competent person

- FENSA or CERTAS certificates for windows

- planning permission for any major work carried out

- building regulation completion certificates and builder’s guarantee certificates for alterations or additions

- subsidence guarantees/warranties

- damp guarantees/warranties

- party wall agreements (if relevant)

- if a listed building, listed building consent for interior and exterior works

- if your home is in a conservation area, conservation area consent for works

- any title insurance policies you may have taken out to solve title defects

Get your home ready

You’ll want to spend some time de-cluttering and making your home look as presentable and attractive as possible, so that as soon as you’ve instructed your agent they can get straight to work.

The quality of the photos that appear on Rightmove play a big part in determining the level of interest the property will get. Low quality photos of cluttered and messy rooms put some people off, whilst high-resolution images of bright, tidy, well-presented homes are attention magnets.

Here are some ideas to make your home look amazing when it’s on display:

- Make it light and airy

Darker rooms generally look smaller than lighter ones, and this can be a big turn off for potential buyers. So we’d suggest making sure that blinds are open, and curtains are apart, to flood your home with light.

- Keep the garden tidy

The front garden is the first thing that a potential buyer will see, so make sure that you give them a reason to smile straight away.

Similarly, the back garden can be a deal clincher, and an impressive outdoor space could set your home apart from the rest. Here are some suggestions for things to tick off your list:

- Bathrooms and kitchens

These two rooms are the most expensive for a buyer to upgrade. However, if you’ve made an effort to clean and declutter them, you’ll be giving potential buyers another reason to be positive about your home. So, here are some of our top tips:

Bathroom:

- Making this room mould-free is a must

- Store toiletries away where possible

- Clean shower doors

- Keep the toilet seat down

Kitchen:

- Keep worktops tidy

- Keep utensils organised and food in cupboards

- Put washing up away

- Clean the windows

- Tidy away any indication of pets being in the house, as your prospective buyer may not be a pet lover

The announcement of a third national lockdown was difficult news for many to hear at the start of this new year, but hopefully the following information will put you at ease with what you can expect from us during this difficult time. We have always, and will always take the steps needed to ensure the safety of our staff and clients – it’s our number one priority. Within the new guidance, you can still move home and attend viewings, and our teams continue to work in a Covid-safe manner.

Before the property viewing:

• V&H Homes employees will check that everyone involved in the visit is feeling well, and if anyone has been experiencing Covid-19 symptoms in the last 14 days, the visit will be postponed

• It will be requested that a maximum of two people (from one household) plus a V&H Homes representative are present at viewings

• V&H Homes will ask the occupant or owners to ensure the property is well ventilated and door are open prior to a visit

• V&H Homes will not be able to provide transport to or from the property

During the property viewing:

• V&H Homes representatives will maintain a 2m distance during the visit with everyone present

• If the property is not large enough to maintain two metres distance, a ‘one in one out’ policy will apply

• Antibacterial gel will be used on arrival and during the visit

• V&H Homes will provide disposable gloves and face covering for our staff and any customers visiting the property

• If there is a need to open doors or cupboards, the V&H Homes representative will do this. Customers will be asked not to touch any surfaces inside the property or any pets present

If you are considering selling or letting your property in Ashtead, Leatherhead, Fetcham, Epsom, Bookham or the surrounding areas, call V&H Homes on 01372 221 678

The following information is taken from Rightmove...

"The property market has experienced a mini boom in 2020, and the big question many of you want answered is: will prices continue to rise in 2021?

Whilst we don’t have a crystal ball, we do have the biggest home-hunting audience in the UK, as well as unique insight into future demand for property.

So armed with all that data, we’ve produced a forecast of what we think will happen to property prices in 2021.

Our main prediction is that the recent surge in average asking prices will continue into next year, as the nation’s housing needs are likely to outweigh any economic uncertainty.

Specifically, we forecast a robust 4% national average house price growth in 2021. However, we think that the price rises will be at a slower pace than this year, which finished 6.6% up on 2019.

What can we expect from the property market in 2021?

It will be a busy start to 2021. The New Year is typically a time for resolutions for the year ahead, and many will see it as an opportunity to draw a line under 2020, which may well include a fresh start in a new home for those who have not already acted.

Many of you have already done so this year, and many more are continuing to do so despite the seasonally quieter run-up to the Christmas period and the declining chance of completing a purchase before the stamp duty deadline in March.

Despite the clock ticking, around 130,000 sales were agreed over the last month, up by a remarkable 44% on the same period in 2019.

However, there remains a processing logjam and some completions are already projected to be delayed until April next year, especially where there are search delays, legal issues or complex mortgage applications.

What will happen when the stamp duty holiday ends?

It will be a slower second quarter once the stamp duty holiday is over, though even with the average price in Britain up by 6.6% this year, cheap mortgage rates that are available for some leave scope for further modest price growth – despite the loss of the tax saving.

What do the experts say?

Rightmove's resident property data expert Tim Bannister explained that it may be quieter in the market in the spring.

He said: “2021 has a lot of variables, and so is not an easy one to call, but with Rightmove’s unique leading indicators of buyer and seller behaviour we are confident that the housing market will continue to outperform general expectations next year as it did this.

“Our 2021 forecast of a 4% price rise is more conservative than the unsustainable 6.6% national average seen this year. There’s likely to be a lull in quarter two unless the stamp duty holiday is extended, but for many buyers its removal will not be make or break, though may lead them to reduce their offers to a degree to compensate for the higher tax, and indeed many sellers may be prepared to help to mitigate their buyer’s financial loss.

“First-time buyers will remain largely exempt, so in most cases will be no worse off. The maximum savings of £2,450 in Wales or £2,100 in Scotland are considerably less decisive than the £15,000 available in England for a house costing £500,000 or more, which does however only apply to a small part of the market.”

If you are considering selling or letting your property in Ashtead, Leatherhead, Fetcham, Epsom, Bookham or the surrounding areas, call V&H Homes on 01372 221 678

Traditionally, spring and autumn are the most popular times to sell your house. But this year has been anything but ordinary and with the stamp duty deadline looming, many sellers have put their house on the market already.

If you are selling your home over the coming winter months, here are some tips to help make sure your property stands out.

- Make your home a cosy refuge from the cold. Put the heating on ahead of viewings and, if you have one, light the fire. Check all your light bulbs, make sure the lights are on throughout the house and consider placing lamps to brighten up any dark corners. For viewings in the late afternoons and evenings, ensure outside lights are on before anyone arrives.

- As ever, promote your home’s best features. With strong demand for home working spaces, showcase how your property fits the bill – whether it’s a separate office or a dedicated desk for home schooling in the playroom. By all means tidy up but don’t feel the need to tidy work away, as it will show off how the space can be used.

- Don’t forget the garden. Outside space is at the top of many buyers’ wish lists so ensure yours is presented in its best light, despite the gloomy winter weather. Make sure it looks cared for by raking up leaves, clearing guttering, mowing the lawn, trimming shrubs, clearing moss from paths and tidying plant pots, removing any weeds. Don’t forget to cut back plants growing around windows so they’re not blocking the light. Put away garden furniture unless it’s a dry, sunny day when you could get it out for viewings.

- As is the case with selling at any other time of the year, make sure your home is clean, decluttered and tidy, and finish off any odd jobs around the house that need doing. Tidy up paintwork and fix damp patches, superficial cracks or stains on ceilings or walls left by previous leaks. This sort of upkeep is typically inexpensive to sort out but can be off-putting on a viewing.

- First impressions count. The front door can get dusty and dirty at this time of year, especially if you live in a town. Keep it washed down and polish any brass door furniture. A collection of pots full of winter flowers by the front door is a welcoming touch and will brighten things up.

If you are considering selling or letting your property in Ashtead, Leatherhead, Fetcham, Epsom, Bookham or the surrounding areas, call V&H Homes on 01372 221 678

As we come to the end of the second lockdown, the government has announced a few changes to the three-tier system that was in place previously in England.

This means that there could be different sets of restrictions that apply depending on where you live.

You may be planning on moving home soon, or perhaps are right in the middle of a move, and would like to know if or how you can still carry on with your plans.

Read on for the latest lowdown, but the short version is that the housing market remains open across all of the UK.

How do local tiers affect my move?

The good news is that the housing market is open and operating irrespective of what tier you’re in.

This means you’re totally free to move homes if you want to – as long as you’re not self-isolating or quarantining.

There are some guidelines for home-moving that apply everyone across the country. Here’s a quick recap of some of the most important ones to keep in mind:

Viewings

Try to do a virtual viewing first, if it’s an option. It’ll reduce the number of viewings agents do, which also minimises the spread of germs.

It could also save you time, because you’ll have a better idea of whether a house is worth seeing or not.

When viewing a property in person, make sure you wear a face mask, avoid touching surfaces, and wash your hands or use sanitiser before and after.

There shouldn’t be more than two households within the property at any one time, and viewings should only be arranged by appointment, so ‘open houses’ aren’t happening at the moment.

If you’re selling your home and are having interested buyers come around to have a look, open all the inside doors beforehand so they don’t have to touch the door handles.

It’s recommended that you’re not in the property during the viewing, and that you disinfect all surfaces after.

Offers through to completion

You’re free to make or accept an offer or reserve a property as normal.

But it’s possible that in some areas the conveyancing process will be slower than usual, as some solicitors and agents may be operating at limited capacity, or are very busy working through deals that have stacked up since earlier in the year.

If you are about to enter into a legally binding contract, you should discuss the possible implications of one of the parties being affected by having to self-isolate or quarantine. Ask your legal representative if they can include provisions to manage these risks in the contracts.

If someone in your household – or the other party’s – began to show any flu symptoms just as you’re about to complete, you’ll probably need to postpone things by a few weeks.

The government says we should all remain flexible in this sort of scenario, so it would be ideal if your contracts can reflect that.

Moving

Removal firms are able to carry out work, as long as all the usual procedures that ensure everyone’s safety are in place.

Try to do most of your packing yourself, if possible. And if you can, give your belongings a quick spray or wipe-down with a disinfectant before they’re handled by someone else.

When the removals’ team is around, do your best to maintain distance and wash your hands regularly.

We also recommend that you book your removals company as early as possible. In many areas they are very busy and if may be a challenge for you to find one available at a short notice.

There are more details within the guidance, but the government has said that the three most important rules, irrespective of what tier you’re in, continue to be:

- Wash your hands – with soap, regularly, and for at least 20 seconds.

- Cover your face – especially when in an enclosed space with people you don’t usually meet with, and where socially distancing is difficult.

- Social distancing – stay two metres apart as much as possible.

If you are considering selling or letting your property in Ashtead, Leatherhead, Fetcham, Epsom, Bookham or the surrounding areas, call V&H Homes on 01372 221 678

The government has announced that the new Help to Buy Equity Loan scheme in England, which is due to begin in April 2021, will be open to new applications from the 16th of December.

This may come as good news for first-time buyers struggling to save up for a deposit of more than 10%, at a time when mortgages with a loan-to-value higher than 85% are hard to find.

The new scheme, which is replacing the current one, is set to run for two years, until March 2023.

Here’s a quick overview of what it is, and who it’s for.

What is the Help to Buy Equity Loan scheme?

Back in 2013, as a way to help more people get on to the property ladder, the government launched a scheme which makes it possible for buyers to buy a home with as little as a 5% deposit.

Close to 300,000 new homes were bought using the scheme in the seven years since its launch, and as it comes to an end, the government has created a new, and similar, one to replace it.

If you’re eligible for the scheme, and can prove you have enough saved to cover a 5% deposit, the government will provide a low-interest loan of 20% of the house price (or up to 40%, if you’re in London), and the mortgage provider will lend the remaining balance.

The government loan is interest-free for the first five years. After that, a monthly interest fee of 1.75% will apply, and will increase each year in April in line with the Consumer Price Index (CPI), plus 2%.

Who’s eligible for it?

The new scheme is only available if you meet all of the following requirements:

- You’re a first-time buyer. You – and your partner, if you’re married or in a civil partnership – must not own, or have previously owned, any property or residential land in the UK or abroad.

- You are purchasing a newly built home. And you’ll have to make sure you’re buying the property off an approved developer who is registered with the scheme.

- The property must be your only property and your permanent residence.

- You can demonstrate you have a minimum deposit of 5% of the property’s purchase price, and that you have the means to keep up with the monthly mortgage and Equity Loan repayments.

Is there a limit to the price of the property I can buy using the scheme?

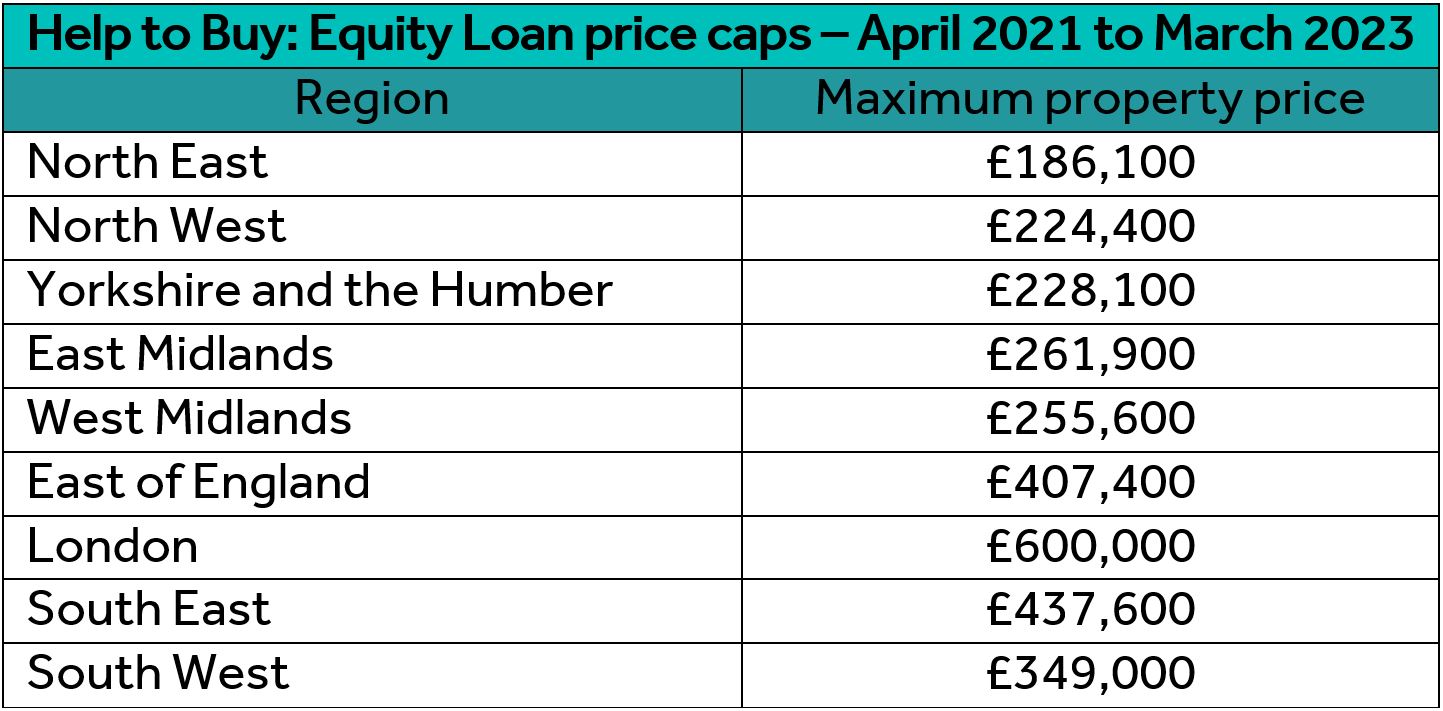

Yes, the government has introduced price caps for each region in England, so the maximum property price will depend on where you are buying.

There are the new regional price caps:

If you are considering selling or letting your property in Ashtead, Leatherhead, Fetcham, Epsom, Bookham or the surrounding areas, call V&H Homes on 01372 221 678