Want to know what your property is worth?

Want to know what your property is worth?

According to tax specialist, Imogen Lea, financial penalties due to ‘seismic’ changes to CGT payment rules could heavily impact people selling buy-to-let properties.

From April 6th, anyone who disposes of a residential property giving rise to a capital gain on which CGT is payable, will be required to make a digital return to HMRC and to pay an estimate of the CGT due within 30 days from the sale completing.

People will also no longer be able to benefit from a possibly substantial sum of money remaining in their hands for up to 22 months after residential property disposal.

Imogen, a consultant in Clarke Willmott’s Taunton private capital team, says: “This is a very big change and could easily catch people out. Interest on the unpaid tax and other financial penalties will be due if the rules are not followed. The risk of such a tight turnaround is people being unaware of the changes and failing to comply. They need to be aware of the vastly reduced time limits and to be ready to make the return and estimate the CGT due.

CGT computations are not always straightforward, which could mean that if people are not prepared, they might not be able to collate the information necessary to make the CGT calculation in time.”

The changes will potentially affect owners of holiday homes, buy-to-let properties, main residences which have been let out at some point, owners of homes with grounds in excess of half a hectare, and owners of houses which have been partly used for business purposes.

Imogen says the changes will not generally apply on the sale of a person’s main residence, but will be relevant on the sale of second homes, and where the main residence exemption does not apply for any reason.

“Gains are not always straightforward to calculate – if an owner has made improvements to the property the cost of these will be deductible from the capital gain, but if there have been numerous improvements over many years it may be challenging for the client to find all the supporting documentation.”

Imogen urges property owners to make an early start of compiling the required information and to start thinking about the CGT position as soon as the property goes on the market.

CGT is calculated by treating the gain as the highest amount of the owner’s income during the tax year in question, and therefore clients will need to estimate their income during the tax year of disposal as this will impact on the CGT rate applicable to the gain.

Personal representatives and trustees, as well as individuals, will be required to comply with the new rules. Meanwhile, gifts of properties also give rise to a disposal for CGT purposes triggering the new requirements.

John Bunker, chair of Chartered Institute of Taxation’s private client UK committee, has branded the new reduced deadline as “a seismic change”.

If you are interested in buying selling or letting a property in Leatherhead, Fetcham, Ashtead, Bookham, Epsom or surrounding areas then please call the office on 01372 221 678 to speak to a member of the team.

We often hear stories of first-time buyers who may not know what to ask or may be too embarassed to ask, what are actually really sensible questions. Hopefully the questions we have collated below should help when it comes to making that all-important decision.

1. Why are the current owners looking to sell the house? This information will help when it comes to putting in an offer. It's good to find out how motivated they are and if they need to move quickly.

2. How long has the house been on the market? The time it takes to sell a property varies depending on local market demand and the price and type of property, so it shouldn't put you off if it's been on for a few months. At the minute, the average time is 63 days from the time a home is added to Rightmove until a buyer is secured.

3. Has the house had any major building works recently? it is reccomended that you have a full structual survey on a property you'd like to buy, but you can ask some questions before then as well.You could ask on the viewing if the house has been extended and how long ago that was. It's also worth asking if there's any potential to extend the property, but bear in mind this will need to through planning permission to may not be approved.

4. What's the parking situation? If your property doesn't come with a garage or parking space, you'll have to work out where you can park and if you need a permit.

5. How much are the utilities? Ask the agent how much the council tax is for the area, and also have a look at the EPC which is available on the property listing to see how energy efficient the house is.

6. Is the property part of a chain? This may give you some bargaining power. If a seller has already found their next property they may be willing to accept a lower offer to secure the sale. However, if they aren't then you might become part of a longer chain so you need to think about how long you're willing to wait.

7. Does the local area have any issues to be aware of? investigating the location propertly is massively important. Do you research. Drive to the house during rush house and ask the neighbours what they think of the area. Also, if you're new to the area and will be commuting by train or bus, try and visit the area both day and night.

8. What's included in the sale? Get as much information as you can here. For exmaple, will any white goods be included?

9. Who are the neighbours? How much this answer affects your decision will vary from buyer to buyer. Noisy neighbours who party all night long could be a massive turn off for some people.

Happy buying!

If you are interested in selling/renting or buying a property within Ashtead,Leatherhead,Epsom,Fetcham,Bookham then please don't hesitate to call the office on 01372 221 678.

Visits to Rightmove surpassed 150 Million for the first time ever on Rightmove in January, making it the busiest ever month ever recorded as home-hunters looked to take advantage of a more vertain political outlook.

There were over 152 million visits to Rightmove in January, a 7% increase on January 2019. The previous record for the busiest month was last set back in May 2019.

The top five busiest days ever on Rightmove were all between 21st and 29th January, with Wednesday 29th topping the list. There were over 5.7 million visits on that day, up 9% on the previous record set back on 24th April 2019.

Time spent by home hunters on the site was up 4%, with people spending a total of 1.17 billion minutes.

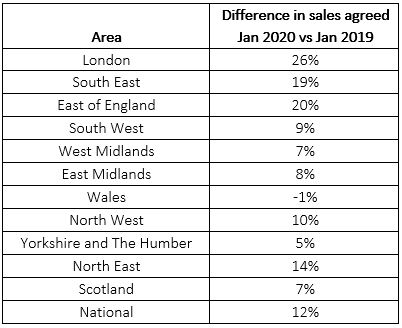

The number of sales being agreed by agents was up 12% compared to the same month in 2019, the biggest year-on-year in any month since July 2017. London saw the biggest uplift, up 26% year-on-year, followed by the East of England, up 20%.

Rightmove's property expert Miles Shipside said: " Home-movers have sprung into action in 2020, with a large number of agents telling us that sales and valuations have picked up significantly in their local areas. There's still an imbalance, with demand growing at a faster rate than new supply and no clear sign yet of any uplift in new listings compared on this time last year, but we could see a new wave of sellings in the coming weeks. The annual jump in sales agreed numbers is the highest we've seen in any month since summer 2016 because of the short-term dip in activity immediately after the Brexit vote. The stage certainly looks set for an active spring if those sellers considering putting their homes up for sale end up doing so, but to catch this wave of buyer momentum sellers should take care not to over-price their homes. It's still a price sensitive market and there's a limit to what buyers can borrow even though mortgage interest rates are temptingly low."

If you are looking to sell/let or buy a property in Ashtead,Leatherhead,Fetcham,Bookham or surrounding areas then please do give the office a call on 01372 221 678.

Many people these days are deciding to improve rather than move. Spiralling costs involved with relocating, low stock levels and economic uncertainty are all playing their part.

But what exactly can you do without planning permission, and is it safe to do it yourself?

Trying to figure out which projects you can do without planning permission can be a bit of a minefield, but don’t panic. As a rule of thumb, most structural changes are subject to building regulations, but some ‘bigger’ renovation projects can be done without planning permission if you adhere to the set size regulations.

Whether you’re building a new structure or making changes to an existing one, you’ll most likely need to submit an architectural drawing of the proposed project and get approval from the local authorities. To clear up the confusion, Comparethemarket.com have teamed up with a range of experts to create a tool that helps you work out which projects require planning permission and what to leave to the professionals.

To be on the safe side, leave any hard wiring and installations to a certified professional. However, if you’re plugging into a socket or wiring into a spur, this can normally be done by any competent amateur. For all other electrical work, you should get it carried out by a trader approved through an appropriate scheme, such as NICEIC.

Chris King, Head of Home at Comparethemarket.com, says: “Anything involving gas is generally best left to certified engineers due to the significant damage which could be caused if you get it wrong.”

Here are five renovations you can do without planning permission.

1: Adding a Porch

You don’t need to apply for planning permission when building a porch if it’s no more than 3 metres above ground level and if the ground floor doesn’t exceed 3 square metres. You also have to make sure that no part of the porch is within 2 metres of any boundary of the house or a highway.

However, if you take the front door of the property out the porch, the porch becomes part of the property and would be subject to building regulations and possibly planning permission.

2: Adding a Conservatory

Planning permissions are not necessary when building a conservatory if you adhere to the strict size regulations. The conservatory should cover less than half of the land surrounding the home, and should not be higher than the highest point of the roof. If the property is a single storey, make sure the conservatory is no higher than 4 metres.

3: Adding a Shed or Summer House

Building regulations do not normally apply to outbuildings, such as an outdoors office or summer house if the floor area of the building is less than 15 square metres and the building is not used for sleeping. The same rules apply to sheds, greenhouses and garages.

However, if the building is between 15 and 30 square metres and doesn’t contain sleeping accommodation, you could get away with no planning permission. To make sure you get it right, it’s always best to check each individual project with the local authorities as architectural drawings may need to be submitted.

4: Adding a Loft Conversion

Unless you live in a designated area, like a national park or World Heritage Sites, loft conversions do not need planning permission as long as the conversion is no higher than the highest part of the roof and made in a similar material to the rest of the house.

If you live in a terraced house, the conversion has a volume allowance of 40 cubic metres of additional roof space or 50 cubic metres for detached and semi-detached houses. Make sure the roof enlargement doesn’t overhang the outer face of the wall of the original house.

5: Putting up a Fence

You will only need planning permission to put up a fence if it’s over 1 metre high next to any highway used by vehicles or the footpath or if it’s over 2 metres high elsewhere. You would also need planning permission if your house is a listed building or in the curtilage of a listed building or if the fence, wall or gate, or any other boundary involved, forms a boundary with a neighbouring listed building or its curtilage.

Need to take down a fence? No planning permission is needed unless the fence is in a conservation area.

Chris warns homeowners about the possible consequences of not doing enough research on your builders: “Make sure you’ve checked their reputation and they have the right liability insurance in place should they damage your property. Most home insurance policies don’t cover poor or faulty workmanship so if the work carried out is poor or unfinished, it’s likely your home insurance wouldn’t be able to step in and come to the rescue.”

If you're interested in buying/selling/renting in Ashtead,Leatherhead,Fetcham or surrounding areas then please dont hestitate to contact the Ashtead office on 01372 221 678

Anyone struggling to sell their home should consider a garden revamp to help make their property more attractive which could be the perfect thing to do in 2020! If you're in Fetcham,Ashtead, Leatherhead or even the surrounding areas and you're looking to sell your property this year, then these following tips could really be useful in how to create a beautiful space which will get you noticed.

Similarly, homeowners who are thinking about putting their property on the market should seriously consider a little green-fingered artistry.

The garden experts at BillyOh.com have mulled over this conundrum and come up with six relatively simple ways to spruce up your outdoor areas.

A spokesperson for BillyOh.com says: “A garden, specifically the front one, is the first impression any prospective buyers of the house will get.

“Treating the garden like any other room of the house will help you make sure it’s working in your favour when the viewings start coming in.

“Although your garden may seem perfect for you and your family, you need to look at it objectively to see what an outsider would think.”

Here are the top six garden transformation tips, according to BillyOh.com:

1. Tidy

If there are piles of rubbish everywhere, this may cause prospective buyers to think this is reflected on the inside of the house. Giving the fence and any furniture a fresh lick of paint will help the space look more welcoming, as viewers visualise themselves and their family in the space.

2. Low maintenance

A low maintenance garden is something which will help sell the house. It means it’s easier for the new owners to put their own identity on the space. Tiered gardens can often put some buyers off, along with big trees which could potentially cause a problem with foundations later down the line.

3. Hedges

If hedges are all trimmed back and neat it will help the space look bigger. Hedges also frame the garden but ensure they don’t look too daunting as you don’t want to offload a large gardening task onto the new owners, who may not be sure on how to look after them.

4. Privacy

No one likes an open garden where all the neighbours can look in. Consider putting up fences or maybe some high hedges to ensure the garden feels like a private extension to the house. An arbour over a seated area could also work for gardens in higher built up areas.

5 . Size

A big, easy to maintain garden is something which many buyers will be looking for. You can make your space immediately look bigger by taking down any children’s toys such as swings or trampolines. You could even consider moving any sheds or greenhouses to ensure the space looks as spacious as possible.

6. Paving

Remember that your garden is not just about the grass and flowers, but also the paving, decking and any other features that come with it. Make sure these have been power-washed down and look clean, and that any cracked paving stones have been replaced.

For Sales & Lettings please call the Ashtead office on 01372 221 678 and we would love to help.

As millions woke up on Fri 13th to the general election result, ‘Property Reporter’ takes a look to see how the property industry has reacted. So, the votes are all in. They have been counted and the UK has spoken. As usual, the property industry was quick to react to the result. Here’s what they are saying:

Saul Empson; Harringtons: “For the wealthy, this is a hugely comforting outcome – they have the party of their choice in power with a majority, and buyers and sellers can all get on with their lives and push forward with the moving plans that they’ve been sitting on for quite some time.”

Nina Harrison; Executive at Haringtons Buying Agency, commented: “I would expect prices to increase – they won’t race up, but prices will definitely strengthen in Central London as more people start to buy and sell again.”

Caroline Takla; Founder of prime London buying agency; The Collection: “Today’s result will be doomsday for a lot of high value deals. I know many buyers who categorically wouldn’t exchange until after the election result, so today, many purchasers and vendors alike will be happy knowing Corbyn’s name is now confined to the history books. A Conservative majority is the outcome most likely to deliver stability and much needed certainty to the market, and one that many of my clients were hoping for. On a local level, there will be more confidence in the market. It will be perceived as a direction of travel. Whilst the precise details of our future relationship with the EU are still not formed, much of the Brexit effect has been priced into the market already. The market will buoy initially, but as these details continue to unfold there will still be buyers who will hesitate before committing.”

Guy Harrington; CEO of property lender Glenhawk: “Finally some light at the end of the Brexit tunnel. This result, coupled with finally leaving the EU in January, is the tonic the real estate market’s been waiting for. Expect improved liquidity, greater transaction volumes, a stronger pound and a bounce in the housing market, all of which will benefit lenders, investors and developers alike.”

Walter Mythen, New Homes Director at JOHNS&CO: “This is the best outcome for the property market, although we anticipate growth will continue to be slow for the foreseeable future as people recover from the hangover of the last three years of political instability. A Tory majority gives us some much-needed clarity and will result in a quicker bounce back to a ‘normal’ market. We wouldn’t expect any dramatic increases or decreases in the market, but buyers and sellers will finally be able to get moving. We may well see the return of the casual investor too – who had all but disappeared in the last three years of political instability.”

Richard Pike at Phoebus Software: “People have voted for a resolutional Brexit, but what does a Conservative majority mean for our Sector? The fact is, a stronger pound, a surge in the money markets and, based on campaign policy, this should be good for all.”

Jamie Johnson; CEO of FJP Investment: “Many will be somewhat relieved with this result – a Conservative majority means we are a step closer to ensuring Brexit will be finalised in some shape or form come the end of January 2020. As expected, there have been some significant movements on the financial markets which is to be expected. Once an election result is announced, the markets will naturally take time to adjust to the news, before once again becoming stable. Of all the possible outcomes to come from the yesterday’s election, a Conservative majority provides the most clarity. Their position on Brexit is clear, and now we wait for Boris Johnson’s EU Withdrawal Agreement to once again be voted on in parliament. Importantly, I hope the government uses this victory to start making progress on national issues that have been ignored; such as the property market.”

Nick Leeming; Chairman at Jackson-Stops, comments: “Over the last few years, both buyers and sellers have done well to adjust to the ongoing uncertainty facing our country, yet we hope that today’s result will finally provide some reassurance to the property market. Throughout the Conservative party’s campaign they pledged their support for greater home ownership and so now is the time for them to form a Government that will deliver on this.

In the lead up to Boris being elected Prime Minister, he spoke widely about stamp duty cuts for UK residents, yet this quickly fell by the wayside as he settled in to No.10. Our latest research found that 41% of consumers think there should be a wholesale reduction in stamp duty across all price brackets, while more than a quarter think Government should abolish stamp duty on all homes under £500,000. Just 3% felt no change was required, which highlights the need for change.

It was therefore disappointing to see the party’s manifesto only focussed on increasing the amount of stamp duty payable for non-UK residents – done in an attempt to take the heat out of the property market. If we are to give the economy the much-needed boost it needs, what we actually need is to reduce the burden of stamp duty across the wider UK housing market.

Although we still have Brexit to contend with, housing must continue to be a key priority for the Conservatives. People are of course still moving. Buying and selling property doesn’t simply stop because the UK is leaving the EU or there has been an election – there are often overriding reasons for moving, whether to be closer to a good school, better childcare or the need to upsize or downsize.

Yet it is quite clear that if our Government wants to see a more fluid property market, which is moving at all levels, then it needs to provide far greater support to key demographics such as first-time buyers, young families and downsizers.”

Paresh Raja, CEO of Market Financial Solutions: “In many ways, today’s result shouldn’t come as much of a surprise. The Conservative Party’s main election pledge has been to ‘get Brexit done’, and the result suggests people are longing for the issue to be resolved come 31stJanuary 2020. What’s more, a majority government means we’re less likely to see a legislative deadlock in Westminster as has been the case since the last election.

For the property market, this is good news. Investors have been yearning for greater certainty and while national house prices have been steadily rising as a result of sustained demand, many have adopted a wait and see approach before committing to a real estate purchase. This result provides some much-needed clarity, and I’d expect to see an increase in property transactions over the coming months.

There are plenty of question marks hanging over the newly-elected government. When will the long overdue budget be delivered? Will there be changes to taxes like stamp duty? How will the housing crisis be addressed? I hope the Prime Minister addresses these questions and does not let Brexit continue to overshadow pressing national issues.

For now, at least, all eyes are turned to the end of January when Boris Johnson’s commitment to deliver Brexit will be put to the ultimate test.”

Jerald Solis, Business Development and Acquisitions Director of Experience Invest: “Despite winning a majority, the Conservative party should view this only as a minor victory. Whilst this was dubbed a ‘Brexit Election’, the public has made it clear that other pressing issues must be pushed to the forefront of the newly elected government’s agenda, such as the housing crisis.

Research from Experience Invest has shown that just 11% of consumers had faith in Boris Johnson’s previous government to solve the problem. So, the question now is how his new government will ensure the appropriate measures are put in place to ensure more people are able to jump onto the property ladder. From the promise to build 29,000 affordable homes, to simplified shared ownership and help to buy loans, the public will be expecting creative action.

One of the main public concerns will now be whether the government will meet the Brexit deadline of 31st January or seek another extension. After all, with over half (53%) of consumers Experience Invest surveyed agreeing that prolonging Brexit is counterproductive to solving the housing crisis, we cannot let Brexit overshadow pressing national issues that have been ignored for far too long.”

Liam Bailey, Global Head of Research at Knight Frank, said: “The Conservative Party has won a majority of just under 80 seats in the UK general election. As a result, the UK is likely to leave the European Union on 31 January, with a vote in Parliament and a Queen’s Speech expected before Christmas.

This will, for the time being, end the uncertainty of a no-deal Brexit and pave the way for the release of some of the pent-up demand that has built in property markets in recent years. The extent to which this translates into transaction activity in the short-term will depend on the size of the pricing expectation gap between buyers and sellers.

Supply is likely to rise as political uncertainty recedes and private and public spending stimulate the UK economy. This will put downwards pressure on prices, however some vendors may expect a bounce in prices, which may create a stand-off between buyers and sellers as the market re-prices.

A shortage of supply in the lettings market may be further exacerbated as owners attempt to capitalise on any perceived ‘bounce’ and list their property on the sales market, which would put upwards pressure on rental values.”

Randeesh Sandhu, CEO of Urban Exposure said:“The Conservative majority delivered at the General Election is the best result for the UK property sector. They are clearly the party that has been and looks set to continue to support home ownership with a series of initiatives in their manifesto focussed on supporting first time buyers, such as the proposed mortgage deposit scheme.

We expect the housebuilding market to also be boosted by a resurgent UK economy in 2020, particularly as and when Brexit is resolved. The RICS survey yesterday showed the property industry believes getting Brexit done will trigger surge in housing market and we very much subscribe to that view. The prospect of a trade deal will have a positive impact across supply chains, as well on demand, as greater certainty breeds improved confidence throughout the sector. Although the timing of any deal is clearly not confirmed, the UK economy and property sector starts from a position of strength, with the ongoing growth in wages outpacing inflation which, in turn, should keep interest rates at record lows. All this adds up to healthy picture for UK housing demand.”

If you own a property in Ashtead, take a look at the table below to see the current average value of properties in your road, the price change over the last 5 years and the number of sales in the last 12 months.

If you are considering moving within or to the village, its useful to know the average prices of your favourite roads!

If you would like an immediate indication as to your properties current value, click on the below link for a free instant online valuation.

Road Name

|

Current AverageValue

|

Price Change5 years (+)

|

Number of saleslast 12 months

|

| Agates Lane | £ 960,749 | £ 229,322 | 0 |

| Albert Road | £ 359,418 | £ 85,802 | 0 |

| Alexander Godley Close | £ 712,799 | £ 170,140 | 0 |

| April Close | £ 712,799 | £ 170,140 | 0 |

| Ashley Cottages | £ 460,229 | £ 109,865 | 0 |

| Ashtead Woods Road | £ 1,115,971 | £ 266,363 | 2 |

| Astede Place | £ 1,126,096 | £ 268,782 | 0 |

| Aston Close | £ 735,657 | £ 175,595 | 0 |

| Bagot Close | £ 570,527 | £ 136,187 | 0 |

| Balquhain Close | £ 304,687 | £ 72,742 | 0 |

| Barnett Wood Lane | £ 625,123 | £ 149,220 | 3 |

| Beechcroft | £ 953,889 | £ 227,684 | 0 |

| Berry Meade | £ 440,959 | £ 105,266 | 2 |

| Berry Walk | £ 921,002 | £ 219,833 | 0 |

| Blacksmith Close | £ 261,613 | £ 62,463 | 0 |

| Bourne Grove | £ 818,381 | £ 195,338 | 0 |

| Bowyers Close | £ 501,324 | £ 119,672 | 3 |

| Bramley Way | £ 544,463 | £ 129,967 | 3 |

| Broadhurst | £ 787,471 | £ 187,966 | 2 |

| Broadmead | £ 236,696 | £ 56,514 | 1 |

| Brookers Close | £ 250,812 | £ 59,883 | 1 |

| Burnside | £ 779,163 | £ 189,484 | 0 |

| Bushey Shaw | £ 680,181 | £ 162,358 | 1 |

| Caenwood Road | £ 435,895 | £ 104,056 | 5 |

| Chaffers Mead | £ 666,188 | £ 159,018 | 1 |

| Chalk Lane | £ 1,528,134 | £ 364,733 | 1 |

| Chantry Close | £ 835,758 | £ 199,488 | 0 |

| Cherry Orchard | £ 975,183 | £ 232,763 | 0 |

| Chestnut Place | £ 1,211,186 | £ 289,091 | 0 |

| Church Road | £ 573,575 | £ 136,917 | 0 |

| Corfe Close | £ 702,357 | £ 167,650 | 0 |

| Craddocks Avenue | £ 634,683 | £ 151,498 | 5 |

| Craddocks Parade | £ 310,617 | £ 74,156 | 0 |

| Crampshaw Lane | £ 1,034,930 | £ 247,023 | 2 |

| Cray Avenue | £ 639,260 | £ 152,591 | 1 |

| Crispin Close | £ 454,356 | £ 108,466 | 1 |

| Culverhay | £ 651,335 | £ 158,401 | 1 |

| Darcy Place | £ 233,396 | £ 55,729 | 0 |

| Darcy Road | £ 506,412 | £ 120,888 | 1 |

| Dene Road | £ 1,037,344 | £ 247,599 | 1 |

| Devitt Close | £ 751,725 | £ 179,435 | 2 |

| Druids Close | £ 1,269,745 | £ 303,066 | 0 |

| Edes Cottages | £ 768,775 | £ 183,502 | 0 |

| Elmwood Close | £ 399,029 | £ 95,255 | 0 |

| Elmwood Court | £ 742,667 | £ 177,276 | 0 |

| Epsom Road | £ 790,914 | £ 188,783 | 0 |

| Fairholme Crescent | £ 655,193 | £ 156,399 | 0 |

| Farm Lane | £ 1,063,952 | £ 258,728 | 1 |

| Floral Court | £ 315,721 | £ 75,375 | 2 |

| Forest Crescent | £ 940,658 | £ 224,525 | 1 |

| Forest Way | £ 661,063 | £ 157,794 | 1 |

| Gayton Close | £ 567,801 | £ 138,093 | 0 |

| Gaywood Road | £ 549,209 | £ 131,100 | 0 |

| Gladstone Road | £ 482,197 | £ 115,109 | 2 |

| Glebe Road | £ 664,594 | £ 158,638 | 0 |

| Grays Lane | £ 1,745,342 | £ 416,576 | 1 |

| Green Lane | £ 624,406 | £ 151,852 | 0 |

| Greville Close | £ 526,461 | £ 125,669 | 0 |

| Greville Park Avenue | £ 1,382,243 | £ 329,918 | 1 |

| Greville Park Road | £ 650,362 | £ 155,240 | 3 |

| Griffin Court | £ 712,799 | £ 170,140 | 0 |

| Grove Road | £ 489,728 | £ 116,904 | 1 |

| Harriotts Close | £ 1,011,530 | £ 241,439 | 1 |

| Harriotts Lane | £ 1,030,378 | £ 245,938 | 2 |

| Hatfield Road | £ 462,387 | £ 110,378 | 2 |

| Highfields | £ 1,059,968 | £ 253,000 | 0 |

| Highlands | £ 796,139 | £ 190,032 | 0 |

| Hillside Road | £ 725,449 | £ 173,164 | 2 |

| Howard Close | £ 712,799 | £ 170,140 | 0 |

| Langwood Close | £ 804,185 | £ 191,955 | 0 |

| Leatherhead Road | £ 661,060 | £ 157,793 | 3 |

| Links Close | £ 696,329 | £ 166,215 | 1 |

| Links Place | £ 712,799 | £ 170,140 | 0 |

| Links Road | £ 785,278 | £ 187,440 | 2 |

| Loraine Gardens | £ 607,933 | £ 145,118 | 0 |

| Maple Road | £ 493,345 | £ 117,770 | 1 |

| Mead End | £ 560,390 | £ 133,773 | 0 |

| Meadow Road | £ 1,151,588 | £ 274,865 | 0 |

| Miena Way | £ 587,643 | £ 142,917 | 0 |

| Moat Court | £ 334,866 | £ 79,944 | 1 |

| Mole Valley Place | £ 594,989 | £ 142,026 | 1 |

| Newton Wood Road | £ 599,053 | £ 143,000 | 5 |

| Northfields | £ 872,267 | £ 208,203 | 0 |

| Oak Way | £ 901,887 | £ 215,272 | 0 |

| Oaken Coppice | £ 1,363,723 | £ 325,496 | 1 |

| Oakfield Road | £ 1,291,092 | £ 308,164 | 0 |

| Oakhill Close | £ 503,500 | £ 120,191 | 1 |

| Oakhill Road | £ 545,516 | £ 130,221 | 2 |

| Old Court | £ 833,665 | £ 198,990 | 0 |

| Oldfield Gardens | £ 935,628 | £ 223,321 | 0 |

| Orchard Drive | £ 840,186 | £ 200,544 | 0 |

| Ottways Avenue | £ 487,564 | £ 116,389 | 0 |

| Ottways Lane | £ 804,858 | £ 192,115 | 3 |

| Overdale | £ 609,482 | £ 145,484 | 4 |

| Paddocks Close | £ 983,920 | £ 234,849 | 0 |

| Paddocks Way | £ 1,060,504 | £ 253,126 | 0 |

| Park Drive | £ 1,250,346 | £ 298,437 | 1 |

| Park Lane | £ 1,352,754 | £ 322,876 | 2 |

| Park Road | £ 722,183 | £ 172,382 | 0 |

| Park Walk | £ 373,561 | £ 89,181 | 1 |

| Parkers Close | £ 704,182 | £ 168,085 | 0 |

| Parkers Hill | £ 1,087,469 | £ 259,562 | 0 |

| Parkers Lane | £ 691,251 | £ 164,999 | 0 |

| Pauls Place | £ 1,142,807 | £ 277,911 | 1 |

| Pepys Close | £ 622,808 | £ 622,808 | 1 |

| Petters Road | £ 629,715 | £ 150,311 | 0 |

| Pleasure Pit Road | £ 1,055,246 | £ 251,870 | 0 |

| Pound Court | £ 435,237 | £ 103,901 | 1 |

| Preston Grove | £ 742,008 | £ 177,113 | 0 |

| Purcells Close | £ 712,799 | £ 170,140 | 0 |

| Quennell Close | £ 645,931 | £ 154,185 | 0 |

| Ralliwood Road | £ 1,490,366 | £ 355,719 | 2 |

| Read Road | £ 428,077 | £ 102,193 | 1 |

| Rectory Close | £ 607,545 | £ 145,025 | 1 |

| Rectory Lane | £ 577,925 | £ 140,551 | 1 |

| Richbell Close | £ 502,155 | £ 119,868 | 0 |

| Roebuck Close | £ 721,837 | £ 172,301 | 2 |

| Rookery Hill | £ 2,140,134 | £ 510,795 | 1 |

| Rosedale | £ 615,551 | £ 146,936 | 0 |

| Rutland Close | £ 421,274 | £ 100,570 | 0 |

| Rye Field | £ 846,987 | £ 202,166 | 0 |

| Shires Close | £ 997,996 | £ 238,208 | 0 |

| Skinners Lane | £ 746,505 | £ 178,188 | 2 |

| South View Road | £ 819,022 | £ 195,495 | 2 |

| St Stephens Avenue | £ 596,862 | £ 142,474 | 1 |

| Stag Leys | £ 639,576 | £ 152,667 | 2 |

| Stonny Croft | £ 472,050 | £ 112,686 | 1 |

| Summerfield | £ 707,925 | £ 168,980 | 1 |

| Taleworth Close | £ 856,192 | £ 208,216 | 0 |

| Taleworth Park | £ 1,104,655 | £ 263,664 | 0 |

| Taleworth Road | £ 777,511 | £ 185,586 | 1 |

| Taylor Road | £ 414,228 | £ 98,885 | 2 |

| The Chase | £ 639,319 | £ 152,609 | 0 |

| The Common | £ 624,436 | £ 149,056 | 0 |

| The Hilders | £ 812,729 | £ 193,992 | 0 |

| The Marld | £ 789,063 | £ 188,346 | 1 |

| The Mead | £ 1,250,333 | £ 298,432 | 0 |

| The Murreys | £ 430,000 | £ 164,381 | 1 |

| The Priors | £ 993,582 | £ 237,154 | 0 |

| The Renmans | £ 621,996 | £ 148,472 | 0 |

| The Ridings | £ 361,732 | £ 86,353 | 2 |

| The Street | £ 277,348 | £ 66,216 | 2 |

| The Topiary | £ 672,028 | £ 160,413 | 0 |

| The Warren | £ 2,527,821 | £ 603,319 | 1 |

| Timberhill | £ 310,735 | £ 74,183 | 0 |

| Uplands | £ 769,022 | £ 183,563 | 0 |

| Virginia Close | £ 572,557 | £ 136,672 | 0 |

| Walters Mead | £ 793,151 | £ 189,321 | 0 |

| Warwick Gardens | £ 688,397 | £ 164,319 | 1 |

| West Farm Avenue | £ 807,172 | £ 196,297 | 1 |

| West Farm Close | £ 674,187 | £ 160,927 | 0 |

| West Farm Drive | £ 803,436 | £ 191,773 | 1 |

| Westfield | £ 517,460 | £ 123,521 | 1 |

| Wishford Court | £ 522,603 | £ 124,753 | 0 |

| Woodfield | £ 509,343 | £ 123,876 | 0 |

| Woodfield Close | £ 390,474 | £ 93,217 | 4 |

| Woodfield Lane | £ 620,969 | £ 148,226 | 1 |

| Woodfield Road | £ 321,326 | £ 76,711 | 0 |

| Woodlands | £ 366,122 | £ 89,052 | 0 |

| Woodlands Copse | £ 954,259 | £ 227,774 | 0 |

| Woodlands Way | £ 875,741 | £ 209,032 | 6 |

As a whole, the average property value in Ashtead is £634,989. This has increased by £177,333 on average over the last 5 years. Safe to say it is a superb area to buy property in!

If you are considering moving, or would simply like an up to date valuation of your home, please call V&H Homes on 01372 221 678 or request a valuation here.